After much back and forth between the House and Senate, both houses passed the TCJA on Dec. 20, 2017 and was signed into law by the President two days later. Thanks to social media and the 24 hour news cycle, we actually got to see how the sausage is made. Not surprisingly, this process proved to not always be pretty. But it is now the law and we are now able to properly plan for it’s impact.

First things first-no you will not be filing each April on a postcard. While the bill was promised as much needed tax simplification it evolved into a wide ranging bill impacting many different income sources of taxable income, deductions and credits. These are but a few of the key takeaways from the bill and how it will affect individual taxpayers starting in 2018 (unless otherwise noted). I will follow with a separate summary for business and investment related changes.

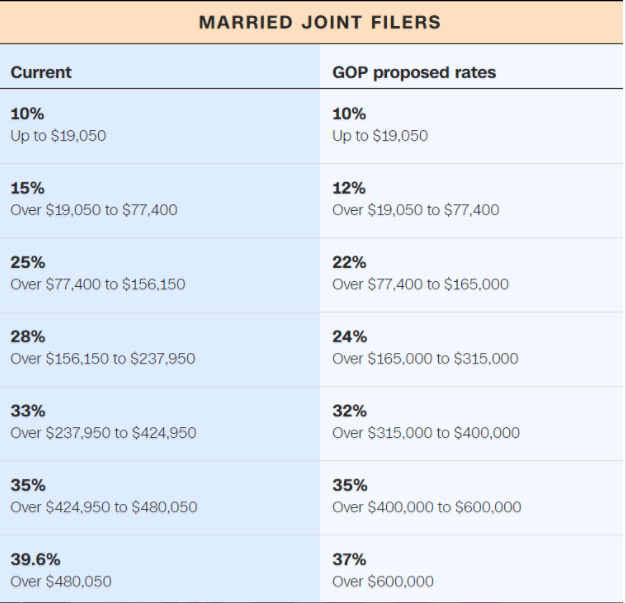

Tax Brackets/Marginal Rates

Almost all taxpayers will enjoy reductions in their marginal rates. 7 brackets remain but the bracket ranges are expanded and the actual marginal tax rates have been reduced by 1-4%. This change alone will be the largest source of tax savings for many taxpayers. As an example, below is a table from CNNMoney that details the tax rate and bracket changes under the previous tax system versus those of the TCJA (GOP proposed rates are the new rates):

Obviously, it is difficult to ascertain every taxpayer’s situation from this one chart but my expectation is that nearly all taxpayers will realize lower tax burdens simply due to the reduced rates and expanded brackets.

Standard Deduction/Personal Exemptions

Starting in 2018 gone are the personal exemptions that have been a mainstay of the tax code for many, many years. Rather, these exemption deductions have been merged into an expanded and increased standard deduction. Effectively, this will leave fewer taxpayers to worry about itemizing their deductions. Beginning in 2018, the standard deduction will be $24,000 for married filing joint and $12,000 for single filers.

Expanded Child Tax Credit

Because of the loss of personal exemptions, taxpayers are now eligible for a larger child tax credit of $2,000 per qualifying child. In addition, more taxpayers will be eligible as the income limitation for married taxpayers is increased from $110,000 to $400,000. This is a big win for taxpayers with children under 17 that previously did not qualify for this credit.

Itemized Deductions

There have been multiple changes to itemized deductions as follows:

- State and Local Tax (SALT)-With much fanfare and consternation taxpayer’s total deduction for SALT (including real property taxes) will now be capped at $10,000. Note: this is only for personal use real property taxes. Rental properties and properties used in trade or business will not have capped deduction amounts.

- Medical Expenses-These appeared on the way out as a deduction all the way up to the passage of the bill. However, the final bill actually EXPANDED the medical deduction RETROACTIVELY for 2017 AND 2018 by requiring only a 7.5% of AGI threshold be met. After 2018, medical expense deduction will revert to the previous 10% of AGI threshold requirement.

- Miscellaneous Itemized Deductions-Starting in 2018 miscellaneous itemized deductions will no longer be allowable. These will include: unreimbursed employee business expenses (mileage, etc.), financial advisory fees (ughhhh), tax preparation fees (double ughhhh), union dues, etc.

- Charitable Contributions–There were no major changes to charitable contributions. However, the fact that fewer taxpayers will be itemizing gives rise to a planning opportunity:

Planning Opportunity: If you are taking Required Minimum Distributions (RMD) but do not expect to itemize deductions (or even if you do) you should consider using your RMD to fund charitable contributions. This has the effect of keeping that RMD amount out of your taxable income.

Primary Mortgages/2nd Residences/Home Equity Lines of Credit

You’ll notice I didn’t include mortgage interest in the changes to itemized deductions. That’s because there were a number of changes surrounding mortgage interest and home ownership in general that warrants its own review. Below is a table that highlights the changes and their implementation.

| Old Law | New Law | Grandfathered? | Comments | |

| Primary Mortgage Interest | Mortgage interest on up to $1M of mortgage principal may be deducted | Mortgage interest on up to $750k of mortgage principal may be deducted | Yes; Mortgages in place prior to 12/15/17 retain the old deductibility rules | |

| Home Equity Indebtedness (HELOCs, etc) | Interest on up to $100k of home equity indebtedness was deductible regardless of use of funds | Home Equity Indebtedness no longer deductible | No; even existing home equity loans lose deductibility starting 1/1/2018 | If the use of funds is for substantial improvement to your primary residence there may still be an allowable deduction |

| 2nd residence mortgage interest | Mortgage interest deductible but constrained by the $1M principal cap | Mortgage interest deductible but constrained by the $750k principal cap | Yes | |

| Primary Residence Gain Exclusion | Can exclude $250k/person for a property that you have resided in 2 of the last 5 years | Unchanged | This was to have been changed but at last minute current law was retained |

Alternative Minimum Tax (AMT)

Originally thought to be on the way to the trash pile (yah!!) AMT ultimately survived (booo!) but in a scaled back way with a significantly larger AMT exemption. In addition, since many of the adjustments that drove AMT scenarios are eliminated (SALT primarily) far fewer taxpayers will deal with AMT starting in 2018. An added bonus: taxpayers with Minimum Tax Credit carryforwards will be able to finally utilize those credits once they are out of AMT. My gut is that very few taxpayers will be subject to AMT at all starting with the 2018 tax year.

Other Tax Items

Here are a few other items that changed or survived this round of tax reform:

- $250 teacher supply deduction SURVIVED though it was rumored to be eliminated.

- 529 proceeds can now be used for elementary and secondary private school expenses (up to a max $10k distribution per student each year)

- Moving Expenses are no longer deductible and employer paid moving expenses are now taxable.

- Entertainment expenses are no longer deductible at all. Meals retain the previous 50% deduction.

- Plug-In Vehicle Tax Credits made the final cut though it was rumored they would be eliminated.

- The health care individual mandate is no longer in effect starting in 2019. Thus tax penalties for failure to have health insurance coverage will no longer apply.

- Alimony tax treatment is reversed meaning payments are not tax deductible and receipt of alimony is not taxable. This new treatment will go into effect 1/1/2019 and prior agreements are grandfathered in to the old rules.

This is a lot. If it seems overwhelming or confusing, well, that’s because it is. Feel free to contact us if you would like to understand how these changes will impact your tax picture.